Private LTE & 5G Network Infrastructure an $8 Billion Opportunity, says SNS Telecom & IT

Industry: Technology

Dubai, UAE (PRUnderground) October 22nd, 2019

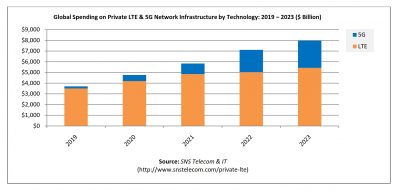

SNS Telecom & IT‘s latest research report indicates that annual investments in private LTE and 5G network infrastructure – which includes RAN (Radio Access Network), mobile core and transport network equipment – will reach $8 Billion by the end of 2023.

With the standardization of features such as MCX (Mission-Critical PTT, Video & Data) services and URLCC (Ultra-Reliable Low-Latency Communications) by the 3GPP, LTE and 5G NR (New Radio) networks are rapidly gaining recognition as an all-inclusive critical communications platform for the delivery of both mission and business critical applications.

By providing authority over wireless coverage and capacity, private LTE and 5G networks ensure guaranteed and secure connectivity, while supporting a wide range of applications – ranging from PTT group communications and real-time video delivery to wireless control and automation in industrial environments. Organizations across the critical communications and industrial IoT (Internet of Things) domains – including public safety agencies, militaries, utilities, oil & gas companies, mining groups, railway & port operators, manufacturers and industrial giants – are making sizeable investments in private LTE networks.

The very first private 5G networks are also beginning to be deployed to serve a diverse array of usage scenarios spanning from connected factory robotics and massive-scale sensor networking to the control of AVGs (Automated Guided Vehicles) and AR/VR (Augmented & Virtual Reality). For example, Daimler’s Mercedes-Benz Cars division is establishing a local 5G network to support automobile production processes at its “Factory 56” in Sindelfingen, while the KMA (Korea Military Academy) is installing a dedicated 5G network in its northern Seoul campus to facilitate mixed reality-based military training programs – with a primary focus on shooting and tactical simulations.

In addition, with the emergence of neutral-host small cells, multi-operator connectivity and unlicensed/shared spectrum access schemes, the use of private LTE and 5G networks in enterprise buildings, campuses and public venues is expected to grow significantly over the coming years. The practicality of spectrum sharing schemes such as the three-tiered CBRS (Citizens Broadband Radio Service) framework and Japan’s unlicensed sXGP (Shared Extended Global Platform) has already been proven with initial rollouts in locations such as corporate campuses, golf courses, race tracks, stadiums, airports and warehouses.

A number of independent neutral-host and wholesale operators are also stepping up with pioneering business models to provide LTE and 5G connectivity services to both mobile operators and enterprises, particularly in indoor settings and locations where it is technically or economically not feasible for traditional operators to deliver substantial wireless coverage and capacity.

Expected to reach $4.7 Billion in annual spending by the end of 2020, private LTE and 5G networks are increasingly becoming the preferred approach to deliver wireless connectivity for critical communications, industrial IoT, enterprise & campus environments, and public venues. The market will further grow at a CAGR of 19% between 2020 and 2023, eventually accounting for nearly $8 Billion by the end of 2023.

SNS Telecom & IT estimates that as much as 30% of these investments – approximately $2.5 Billion – will be directed towards the build-out of private 5G networks which will become preferred wireless connectivity medium to support the ongoing Industry 4.0 revolution for the automation and digitization of factories, warehouses, ports and other industrial premises, in addition to serving other verticals.

The “Private LTE & 5G Network Ecosystem: 2020 – 2030 – Opportunities, Challenges, Strategies, Industry Verticals & Forecasts” report presents an in-depth assessment of the private LTE and 5G network ecosystem including market drivers, challenges, enabling technologies, vertical market opportunities, applications, key trends, standardization, spectrum availability/allocation, regulatory landscape, deployment case studies, opportunities, future roadmap, value chain, ecosystem player profiles and strategies. The report also presents forecasts for private LTE and 5G network infrastructure investments from 2020 till 2030. The forecasts cover three submarkets, two air interface technologies, 10 vertical markets and six regions.

The key findings of the report include:

- Expected to reach $4.7 Billion in annual spending by the end of 2020, private LTE and 5G networks are increasingly becoming the preferred approach to deliver wireless connectivity for critical communications, industrial IoT, enterprise & campus environments, and public venues. The market will further grow at a CAGR of 19% between 2020 and 2023, eventually accounting for nearly $8 Billion by the end of 2023.

- SNS Telecom & IT estimates that as much as 30% of these investments – approximately $2.5 Billion – will be directed towards the build-out of private 5G networks which will become preferred wireless connectivity medium to support the ongoing Industry 4.0 revolution for the automation of factories, warehouses, ports and other industrial premises, besides serving additional verticals.

- Favorable spectrum licensing regimes – such as the German Government’s decision to reserve frequencies in the 3.7 – 3.8 GHz range for localized 5G networks – will be central to the successful adoption of private 5G networks.

- A number of other countries – including Sweden, United Kingdom, Japan, Hong Kong and Australia – are also moving forward with their plans to identify and allocate spectrum for localized, private 5G networks with a primary focus on the 3.7 GHz, 26 GHz and 28 GHz frequency bands.

- The very first private 5G networks are also beginning to be deployed to serve a diverse array of usage scenarios spanning from connected factory robotics and massive-scale sensor networking to the control of AVGs (Automated Guided Vehicles) and AR/VR (Augmented & Virtual Reality).

- For example, Daimler’s Mercedes-Benz Cars division is establishing a local 5G network to support automobile production processes at its “Factory 56” in Sindelfingen, while the KMA (Korea Military Academy) is installing a dedicated 5G network in its northern Seoul campus to facilitate mixed reality-based military training programs – with a primary focus on shooting and tactical simulations.

- The private LTE network submarket is well-established with operational deployments across multiple segments of the critical communications and industrial IoT (Internet of Things) industry, as well as enterprise buildings, campuses and public venues. China alone has hundreds of small to medium scale private LTE networks, extending from single site systems through to city-wide networks – predominantly to support police forces, local authorities, power utilities, railways, metro systems, airports and maritime ports.

- Private LTE networks are expected to continue their upward trajectory beyond 2020, with a spate of ongoing and planned network rollouts – from nationwide public safety broadband networks to usage scenarios as diverse as putting LTE-based communications infrastructure on the Moon.

- In addition to the high-profile FirstNet, South Korea’s Safe-Net, Britain’s ESN (Emergency Services Network) nationwide public safety LTE network projects, a number of other national-level engagements have recently come to light – most notably, the Royal Thai Police’s LTE network which is already operational in the greater Bangkok region, Finland’s VIRVE 2.0 mission-critical mobile broadband service, France’s PCSTORM critical communications broadband project, and Russia’s planned secure 450 MHz LTE network for police forces, emergency services and the national guard.

- Other segments within the critical communications industry have also seen growth in the adoption of private LTE networks – with recent investments focused on mining, port and factory automation, deployable broadband systems for military communications, mission-critical voice, broadband and train control applications for railways and metro systems, ATG (Air-to-Ground) and airport surface wireless connectivity for aviation, field area networks for utilities, and maritime LTE platforms for vessels and offshore energy assets.

- In the coming months and years, we expect to see significant activity in the 1.9 GHz sXGP, 3.5 GHz CBRS, 5 GHz and other unlicensed/shared spectrum bands to support the operation of private LTE and 5G networks across a range of environments, particularly enterprise buildings, campuses, public venues, factories and warehouses.

- Leveraging their extensive spectrum assets and mobile networking expertise combined with a growing focus on vertical industries, mobile operators are continuing to retain a strong foothold in the wider private LTE and 5G network ecosystem – with active involvement in projects ranging from large-scale nationwide public safety LTE networks to highly localized 5G networks for industrial environments.

- A number of independent neutral-host and wholesale operators are also stepping up with pioneering business models to provide LTE and 5G connectivity services to both mobile operators and enterprises. For example, using strategically acquired 2.6 GHz and 3.6 GHz spectrum licenses, Airspan’s operating company Dense Air plans to provide wholesale wireless connectivity in Ireland, Belgium, Portugal, New Zealand and Australia.

- Cross-industry partnerships are becoming more commonplace as LTE/5G network equipment suppliers wrestle to gain ground in key vertical domains. For example, Nokia has partnered with Komatsu, Sandvik, Konecranes and Kalmar to develop tailored private LTE and 5G network solutions for the mining and transportation industries.

The report will be of value to current and future potential investors into the private LTE and 5G network ecosystem, as well as LTE/5G infrastructure suppliers, critical communications organizations, industrial IoT companies, vertical-domain specialists, mobile operators, MVNOs, neutral hosts and other ecosystem players who wish to broaden their knowledge of the ecosystem.

For further information concerning the SNS Telecom & IT publication “The Private LTE & 5G Network Ecosystem: 2020 – 2030 – Opportunities, Challenges, Strategies, Industry Verticals & Forecasts” please visit: https://www.snstelecom.com/private-lte

For a sample please contact:

Email: info@snstelecom.com

Notes for Editors

If you are interested in a more detailed overview of this report, please send an e-mail to info@snstelecom.com

About SNS Telecom & IT

Part of the SNS Worldwide group, SNS Telecom & IT is a global market intelligence and consulting firm with a primary focus on the telecommunications and information technology industries. Developed by in-house subject matter experts, our market intelligence and research reports provide unique insights on both established and emerging technologies. Our areas of coverage include but are not limited to wireless networks, 5G, LTE, SDN (Software Defined Networking), NFV (Network Functions Virtualization), IoT (Internet of Things), critical communications, big data, smart cities, smart homes, consumer electronics, wearable technologies, and vertical applications.